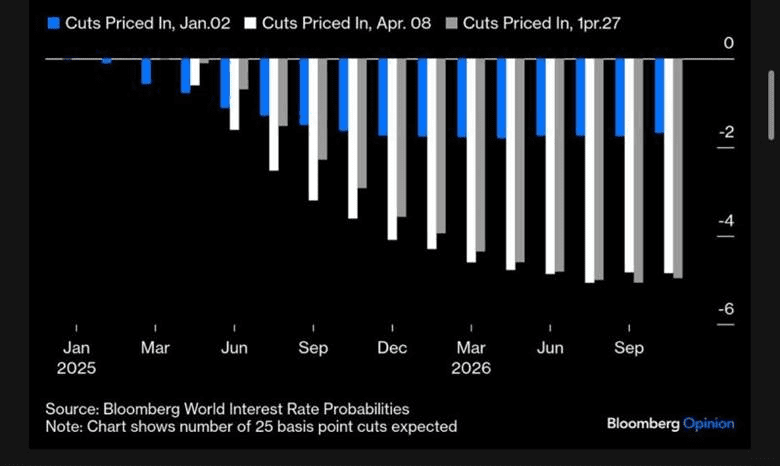

It is often the case that we see periods of market volatility where there is significant divergence between market expectations for policy and the central bank’s actual stance. The chart below shows how market expectations for Fed rate cuts have evolved this year – specifically, what was priced in by markets on January 2, April 8, and April 27. Expectations have grown from two 25-basis-point cuts to five. However, this series of aggressive cuts is unlikely to materialize unless the US economy falls into recession and the unemployment rate rises sharply.

Much of the shift in expectations has been driven by uncertainty surrounding tariffs. Markets have begun to price in expectations of a US recession and lower corporate profits. Tariffs – and the uncertainty they bring – will hit real consumption and investment, which will slow economic growth and raise the unemployment rate. Tariffs will also cause a temporary boost in inflation. However, this won’t lead to persistent inflation unless inflation expectations rise and become embedded in wage and price setting behaviour. While the Fed is unlikely to respond to a policy-induced negative shock, it will likely lower interest rates if unemployment rises.

Adding to the Fed’s policy challenges are growing concerns over the loss of US government credibility and rising US debt burdens – a potentially toxic mix. A material loss of credibility would change investors’ view of US Treasuries as a safe-haven asset, putting both the US debt and current account deficit at risk. Diminished credibility reduces the risk-adjusted expected rates of return on USD-denominated assets and has contributed to a weakening US dollar. Foreigner investors currently hold nearly one-third of all outstanding publicly-held US debt.

Recently, 30-year Treasury yields briefly flirted with the 5 per cent mark, raising concerns about market stability. During a week of intense market turbulence, Fed Governor Susan Collins stated that the Federal Reserve “would absolutely be prepared” to intervene if needed. The sharp decline in the US dollar, coupled with the recent spike in Treasury yields, are major concerns for the Fed, potentially forcing it to take action to restore market stability.

If conditions were to become disorderly, the Fed could deploy its full range of tools to stabilize the bond market. This would likely include injecting liquidity through measures like the Large Scale Asset Purchases (LSAP) or Quantitative Easing (QE).

When the Fed engages in QE, it injects new reserves into the banking system. Adding large amounts of reserves will lead banks to readjust their portfolios. Because reserves are zero-duration, low-yielding assets, banks will want to rebalance toward holding more bonds. This process helps reduce market volatility and compresses credit spreads. In turn, asset allocators and investors take on additional risk in their portfolios, supporting the flow of credit and capital throughout the economy.

Housing Affordability Watch

CMI monitors the latest developments and offers insights on solutions to Canada’s housing affordability crisis

In 2017, CMHC launched a National Housing Strategy, a 10-year, $115 billion plan to make housing affordable for all. Eight years later, the housing crisis remains a key issue. Is the federal government truly capable of building the homes Canadians need?

In our latest Housing Affordability Watch, we examine the challenges facing the government’s housing strategy and whether it can deliver the promised results.

Read it here: Is the Federal Government Capable of Building Homes?

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any person or organization in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice including investment advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication. Readers are cautioned to always seek independent professional advice from a qualified professional before making any investment decisions.