The Large Urban Centre Alliance, representing home builders and rental providers from cities that account for more than 50 per cent of Canada’s annual housing starts, has presented a set of housing recommendations ahead of the federal government’s pre-budget consultations.

The proposal includes four primary and four secondary recommendations. Last week, we examined the primary recommendations. This week, we’re looking at the secondary recommendations (numbered 5 through 10 in the proposal), which aim to speed up and simplify the homebuilding process:

- Tie federal infrastructure funding to pro-housing supply initiatives.

- Implement municipal reforms, including accepting surety bonds in subdivision and site plan agreements and introducing Edmonton-style automated approval programs.

- Enforce the conditions set out in municipal Housing Accelerator Fund agreements.

- Exempt real estate and housing-related infrastructure investment from the EIFEL (Excessive Interest and Financing Expenses Limitation) rules, and review other federal housing-related taxes and regulations, including the mortgage stress test, to ensure they are appropriate for current conditions.

- Launch consultations on the MURB (multi-unit residential building) tax provision this fall, aiming to make rental projects that begin construction on or after January 1, 2026, eligible for the tax provision.

- Create a time-limited incentive for investors who currently own non-purpose-built rental properties to sell and reinvest the proceeds into MURB-eligible projects, and enable condominium construction financing by allowing banks to reduce pre-sale requirements on new condo developments via federal backstop facilities.

Below we examine each of these secondary recommendations in detail.

5. To accelerate the construction of new homes, tie federal infrastructure funding to pro-housing supply municipal reforms, such as accepting surety bonds in subdivision agreements and site plan agreements and implementing Edmonton-style automated approval programs.

These are good recommendations. The challenge is implementation.

Ontario’s new Planning Act came into effect in 2024. Under the previous system, developers were required to provide irrevocable letters of credit (LOCs) or other forms of direct collateral to municipalities to guarantee project completion. This tied up the developer’s credit facility — for example, if a $2 million LOC was issued, that amount would be unavailable for other borrowing, sometimes for the entire duration of a multi-year project.

The new Act allows developers to use surety bonds instead of letters of credit. With a surety bond, the developer pays a premium rather than tying up credit. If a developer is unable to meet its obligations, the insurance provision is triggered, and the surety provider steps in to fulfill them. The key difference – and main advantage – of a surety bond over a letter of credit is that it preserves the developers credit capacity, allowing greater financial flexibility.

As we have noted, CMHC could take the lead in creating a national framework to support the consistent use of this tool.

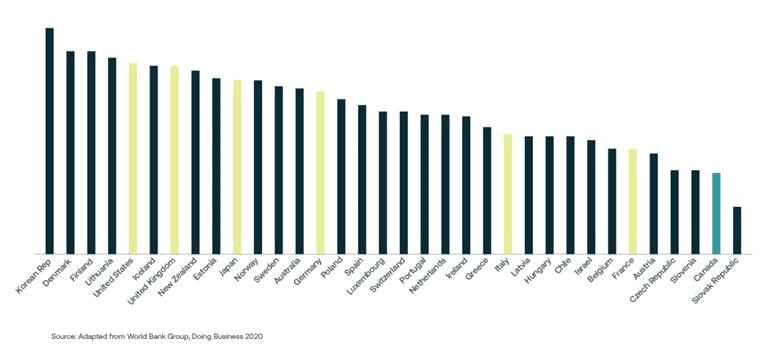

Approval delays are a major cost challenge for builders. Compared with other OECD countries, Canada is one of the slowest jurisdictions in approving new housing projects.

Time score (low = poor)

Source: Altus Group (adapted from World Bank Group, Doing Business 2020)

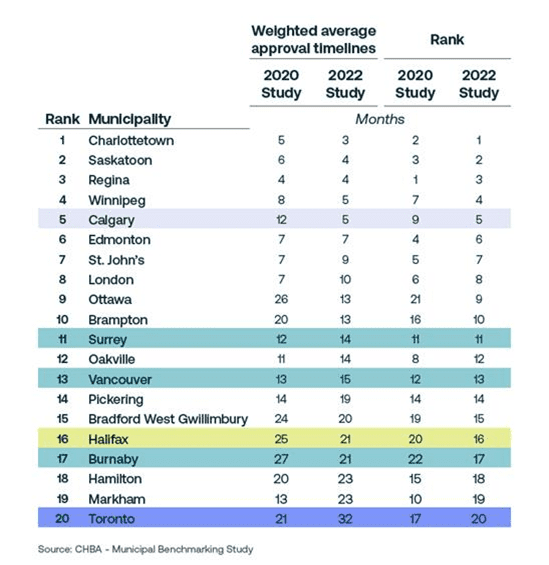

Approvals and permitting delays are particularly acute in major metros such as Vancouver and Toronto. A study by Altus Group, conducted on behalf of the Canadian Home Builders Association, found that the longest delays were in Toronto, where staffing shortages and outdated processes pushed the weighted average approval timeline from 21 months in 2020 to 32 months in 2022.

Source: Altus Group (adapted from CHBA – Municipal Benchmarking Study)

In 2024, Edmonton introduced an automated approval program. Applicants looking to build a single-detached or semi-detached home in a greenfield area (zoned Small Scale Flex Residential) can submit a development application through the city’s Self Service website. If the application meets requirements and isn’t selected for a random audit, the development permit is issued immediately. Builders can also apply online for a partial building permit for footings and foundations – another automated process – and, with same-day approval, begin construction.

Currently, the process is limited to single- and semi-detached homes in a pre-zoned area. It is not yet equipped to approve more complex developments like high-, mid-, or even low-rise multi-unit housing. Still, it shortens the approval timeline significantly – from two weeks to just one day.

The City hopes to expand the system by enabling it to issue permits for more complex projects or to pre-screen applications. This would allow builders to enter their project details and quickly check compliance with regulations and other requirements, helping to speed up the process even further.

It’s a promising approach, but so far other cities have been slow to follow Edmonton’s lead. While tying infrastructure funding to faster approval times is a good idea in theory, implementation is the real challenge. The federal government has shown little appetite for a system with clear, enforceable targets, and it’s unlikely Ottawa would actually pull funding from municipalities. A more practical solution may lie with the provinces, which have the authority under their respective municipalities acts to create approval and enforcement regimes. Without provincial support, this isn’t a workable idea.

6. To lower the price of new homes and increase the diversity of housing options available to Canadians, enforce the conditions set out in municipal Housing Accelerator Fund agreements.

While we agree with this position, the Housing, Infrastructure and Communities Department and its Minister have not enforced these agreements. No action has been taken regarding Toronto moving away from its initial agreement to allow 6-plex development as a right.

As we noted in January, while CMHC is expected to fix these problems, it has limited control over the process. The Housing Accelerator Fund is as much about optics as it is about outcomes, giving MPs an opportunity to announce government funding in their ridings. Policy-making and oversight of the program lie with the Housing, Infrastructure and Communities Department and its Minister. Looking to CMHC to fix this will not work. The Minister and his department negotiated the agreements and should be held accountable for any shortcomings.

Until there is political will to enforce accountability, this program will remain more about political theater than tangible results.

7. To unlock much-needed global capital into housing construction, fully exempt real estate and housing-related infrastructure investment from EIFEL rules, and conduct a full review of other federal housing-related taxes and regulations, including the OSFI mortgage stress test, to ensure they are designed appropriately for the current conditions.

EIFEL limits the deductibility of net Interest and Financing Expenses (IFE), capping them at a 30 per cent fixed ratio of Adjusted Taxable Income (ATI). Any interest amounts denied under these rules can be carried forward, allowing taxpayers to offset them against future taxable income.

These rules have been updated to include an elective exemption for interest and financing expenses related to arm’s length financing of purpose-built rental housing. This exemption applies to financing incurred before January 1, 2036.

The recommendation does not specify where the current rule is constraining housing construction. I agree that if such constraints can be demonstrated, further exemptive relief should be provided.

The other proposal is to review the mortgage stress test. OSFI is already considering alternatives and is evaluating a loan-to-income (LTI) framework until at least January 2026. Similar LTI frameworks exist in other countries, like the UK, where mortgages are capped at 4.5 times borrower income.

8. To build much-needed missing-middle rental housing and to channel investor dollars towards new rental construction, launch consultations on the proposed Multi-Unit Rental Building (MURB) tax provision this fall, with the goal of ensuring that rental projects that begin construction on or after January 1, 2026, are eligible for the tax provision.

9. To increase the capital available for MURB tax provision eligible projects, create a time-limited incentive for investors who currently own non-purpose-built rental properties who sell the units and reinvest the proceeds into a project eligible for the MURB tax provision.

In the US, there are replacement property rules, including the well-known “like-kind exchange” provisions under § 1031 of the US Internal Revenue Code (IRC). Generally, §1031 applies automatically if the following requirements are met:

- There is an exchange of property;

- The exchange is “solely” for like-kind property;

- Both the property exchanged and the property received are held for productive use in a trade or business or for investment; and

- The taxpayer identifies the new property to be received within 45 days and completes the legal transfer of that property within six months of transferring the original property.

Similar provisions in Canada existed prior to the 1970 Income Tax Act reforms, which were instrumental in encouraging the construction of purpose-built rental housing.

Most rental property owners own a condominium. Given the current state of the condo market, investors are finding it increasingly difficult to sell these units – particularly the micro-units targeted at small investors. If this incentive encourages investors to switch from condos, it may not be a good thing for the market: it would add more supply, depress prices further and discourage the construction of new condo units.

“Like-kind exchange” rules are important for encouraging more activity in the rental market, but they should be implemented as a broad policy, not a narrowly-focused, interim measure.

Certainly, the MURB program did help stimulate construction, but it also led to significant investor losses. Most of the initial tax benefits were eroded by changes to tax rules over the life of the program. Activity was often driven primarily by maximizing tax advantages, sometimes leading to practices such as pouring foundations in December just so CMHC could determine that there was a housing start and investors could claim the tax benefits.

For much of the program’s duration, top marginal tax rates for individuals exceeded 60 per cent, meaning investors were often more motivated by tax relief than the underlying economics of the project.

I am skeptical that we will see a significant uptake of MURBs. The tax incentives are less advantageous now than in the past, development timelines are much longer – limiting the potential tax benefit – and provincial securities regulators are likely to scrutinize any proposals, given that investors were previously burned by investing in these structures. In addition, investors now have far more options than they did in the past.

10. To enable condo construction to be financed after small-scale investor dollars have been shifted towards MURB-eligible projects, enable banks to reduce pre-sale requirements on new condo developments via federal backstop facilities.

I doubt that OSFI would support changes to pre-sale rules. While CMHC provided ad hoc support to the condo industry after the financial crisis to make bank financing more accessible, a similar program today would be challenging. The key issues would be how much capital OSFI would require CMHC to hold to support the development of new condos and whether builders could finance the associated insurance premium while delivering condos intended for owner-occupied units rather than rentals.

While each recommendation has merit, the real challenge is execution – an area where all levels of government have been lacking. Without a clear plan to implement these proposals, they may sound promising, but I fear that little will actually be accomplished.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any person or organization in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice including investment advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication. Readers are cautioned to always seek independent professional advice from a qualified professional before making any investment decisions.