The Large Urban Centre Alliance, representing home builders and rental providers from cities that account for more than 50 per cent of Canada’s annual housing starts, has presented a set of housing proposals ahead of the federal government’s pre-budge consultations.

The proposal includes four primary and four secondary recommendations. The primary recommendations are:

- Provide a temporary three-year expansion of the 100 per cent GST/HST rebate on new homes and those substantially renovated up to $1 million, with a partial rebate for homes between $1 million and $1.5 million, while maintaining all other program criteria.

- Protect consumers from unnecessary costs and double taxation by adopting a transparent billing model where municipal development charges are billed directly to buyers rather than embedded in builders’ costs.

- Adjust the foreign buyer ban to unlock required capital for construction by adopting an Australian-type of model and extend the GST/HST exemption to purpose-built rental projects under construction.

- Ensure CMHC’s Apartment Construction Loan Program (ACLP) is sufficiently capitalized to meet growing demand.

In this note, we examine some of the issues related to the primary recommendations. While some of the proposals have merit, others require further analysis.

1. Expanding the new GST/HST rebate

When the GST was implemented, the expectation was that the relief for new housing would be reviewed and adjusted as house prices rose over time. This was never followed through on until the most recent federal budget. The budget proposal applies to purchase and sale agreements entered into after May 26, 2025, and before 2031.

The Alliance is calling for a 3-year extension of the rebate. The rationale for the 3-year period is unclear. I assume it’s intended to provide builders with a reasonable planning horizon, given the length of the development process. Ultimately, this recommendation is less about a new policy direction and more about ensuring the government lives up to the original intent of the GST framework.

Ideally, when a buyer purchases a new property, the GST/HST rebate is assigned to the builder upon closing. The builder then uses the rebate to reduce the purchase cost of the property. This portion of the GST/HST is therefore not added to the purchase price, and the builder subsequently applies for the GST/HST rebate for the property.

If the GST/HST exemption is extended to purpose-built rental projects under construction, we would expect a similar push to expand this treatment to rental properties more broadly, beyond the current rebates available. The benefit would be twofold: it would remove some of the onus on the builder to determine if the buyer intends to reside in the property rather than rent it out, and it would improve the economics of condo rentals.

2. Transparent billing

Currently, development charges (DCs) are paid up front by the developer. These charges – along with the cost of financing them and any associated GST/HST (since the cost is included in the sale price) – are ultimately paid by the borrower. The argument is that if the borrower paid the DCs directly at closing, the costs would be more transparent and potentially lower, as the borrower would avoid paying both the builder’s carrying costs on the DC payment and the indirect taxes on those charges.

The assumption is that the buyer/borrower could fund this cost as part of the mortgage. In practice, they effectively do, since DCs are embedded in the purchase price. However, a mortgage statement of adjustments shows that taxes are not normally financed: the buyer must reimburse the seller for any property taxes the seller prepaid, and provincial land transfer taxes are paid separately.

This raises the question of whether, if DCs were charged directly to the borrower, lenders would be willing to finance them. I struggle to see why they would. While the cost is currently financed indirectly as part of the purchase price, once separated into its own line item, it would likely fall outside the scope of expenses typically eligible to be financed through mortgage proceeds.

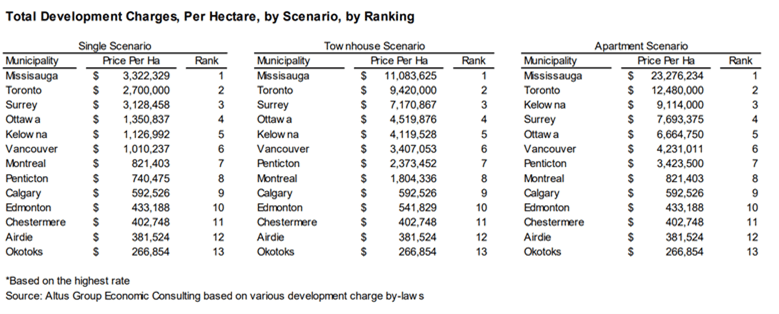

The bigger issue is that, in BC and Ontario, DCs have become a key source of municipal revenue. Rather than perpetuating this problem, it would make more sense for the provinces to deal with this directly. As the table below makes clear, this is not a national issue. It should be dealt with on a regional basis rather than involving the federal government in problems faced by just a few provinces.

Source: Altus Group Economic Consulting

Note: this study compares infrastructure charges across three development scenarios that could potentially occur on one hectare of land: a development of 27 single-family homes (detached or semi-detached); a development of 113 townhouses; and a development of 250 apartment units.

3. Foreign buyer ban

Adjusting the foreign buyer ban to adopt an Australian-style model would primarily benefit the condo construction market. Even if the federal government removed the ban, BC and Ontario have their own foreign buyer restrictions. BC Premier Eby has essentially dismissed this proposal as a non-starter. Without provincial support, the federal government has no reason to pursue this option.

Moreover, public support for removing the ban is limited. According to a survey by Research Co., about 76 per cent of Canadians support the federal ban on foreign real estate purchases, which is currently in effect until January 1, 2027. The poll shows broad consensus across the political spectrum, with 82 per cent of Conservative voters and 78 per cent of both Liberal and New Democrat voters supporting the policy.

While preconstruction financing challenges for condos have been partly attributed to a lack of foreign buyers, the more significant issue is banks’ reluctance to lend in the current environment. Potential solutions for addressing this will be discussed in a follow-up note on secondary recommendations.

If the builders believe that the foreign buyer ban restricts the flow of foreign capital for financing housing development and construction, that issue should be addressed directly rather than by removing the ban.

4. CMHC’s Apartment Construction Loan Program (ACLP)

This program has evolved from a temporary measure into the main financing source for purpose-built rentals. Industry demands highlight that lenders need long-term, subsidized financing to make these rental projects viable. If government support is to be provided, it makes sense to consider whether there are other more effective ways to deliver it.

Prior to changes in the Tax Act in the early 1970s, the tax system favoured rental construction such that this activity required no special government funding. If we are going to support rental housing today, we need to determine the optimal approach – whether through tax policy changes, subsidized lending or a combination of both. The ACLP was established because Finance was against changes to tax policy. However, I have never seen a study comparing the two policy solutions.

If the government continues to heavily fund the ACLP program, it creates significant concentration risk, positioning CMHC as the primary construction financing provider nationally (we seem to have forgotten the commercial real estate crisis of the 1980s and 1990s). Any major economic downturn would expose CMHC to significant completion risk. While CMHC has attempted to modify the program to manage this risk, these adjustments are a second-best solution, as the risk remains concentrated with CMHC.

Another challenge CMHC faces is a lack of operational expertise. When the ACLP program was launched, it was not intended to be permanent, and the underwriting and servicing of loans were contracted out to the private sector. To better manage risk, CMHC needs to develop this expertise internally.

It is encouraging to see the development community preparing a national proposal, but it reads more like a Christmas wish list than a detailed policy analysis. Next week, we’ll take a closer look at the proposal’s secondary recommendations.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any person or organization in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice including investment advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication. Readers are cautioned to always seek independent professional advice from a qualified professional before making any investment decisions.