Almost everyone takes out a loan to buy a home. As the loan is being paid back, you build up the equity in your home. Home equity is the difference between the market value of your home and what you owe that bank on the loan.

For example, if your home has a market value of $500,000 and you currently owe the lender $300,00, then you have $200,000 worth of equity. Here is how home equity applies to your situation, and how a home equity loan may help.

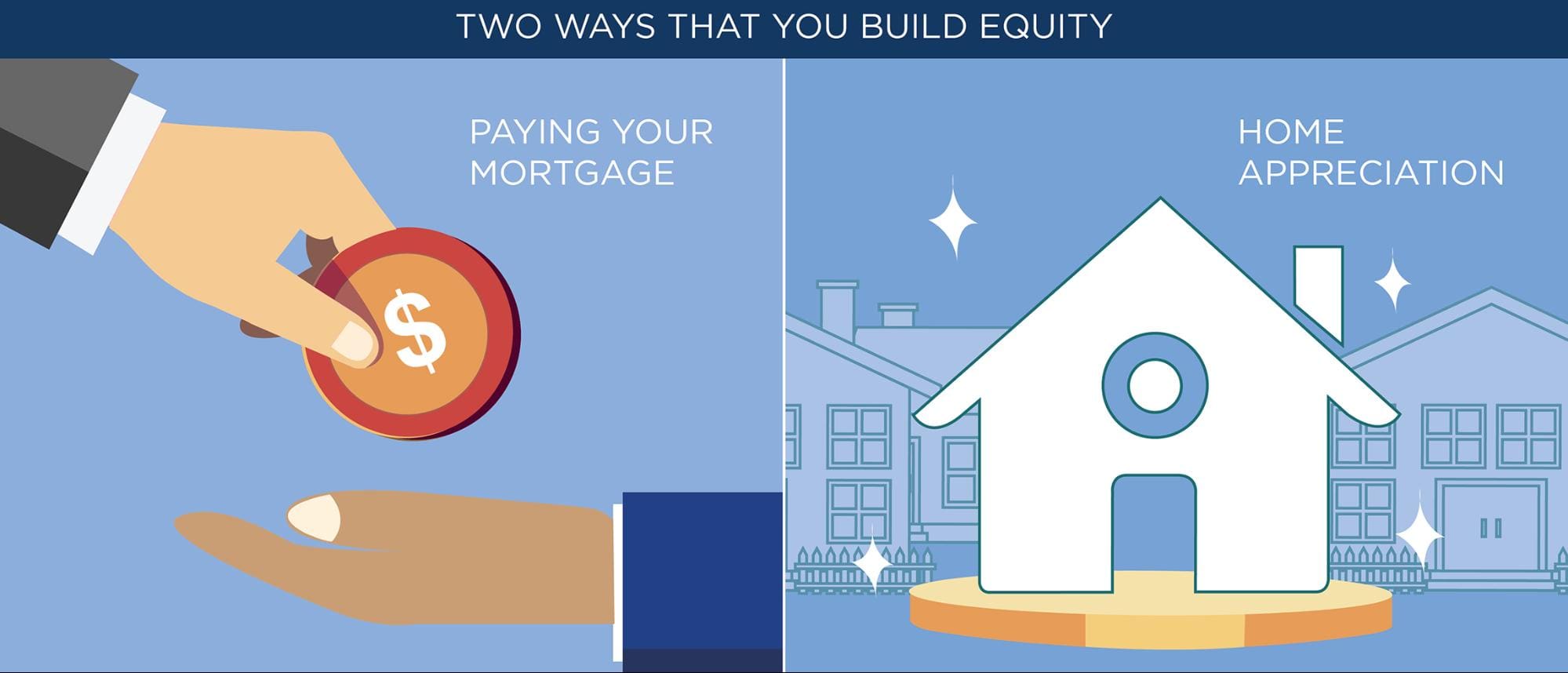

How do you build equity in your home?

There are two ways that you build equity. The first involves the paying back of the mortgage. Every month when a payment is made to your lender, you reduce a portion of your principal.

Your principal is the amount of money you borrowed from the lender while the balance of your payment goes to paying the interest. At the beginning of your payment term (i.e., first few years), most of the payments you make on a monthly basis goes towards the interest payments.

Over time, your payments go towards your principal rather than the interest. The more you reduce the principal amount outstanding, the more equity you have in your home.

Some mortgages are structured in a way that allows you to make extra payments toward the principal each month. This reduces the amortization term of your mortgage (number of years you have to make mortgage payments) and helps you build equity faster.

The other way that equity accumulates within your home is the value increase of your home. If your home is worth more now compared to when it was purchased, your home gains equity. When your home appreciates in value as a result of market conditions and when you make improvements to your home, that extra bump in value further helps boost your home equity.

Home equity: A case example

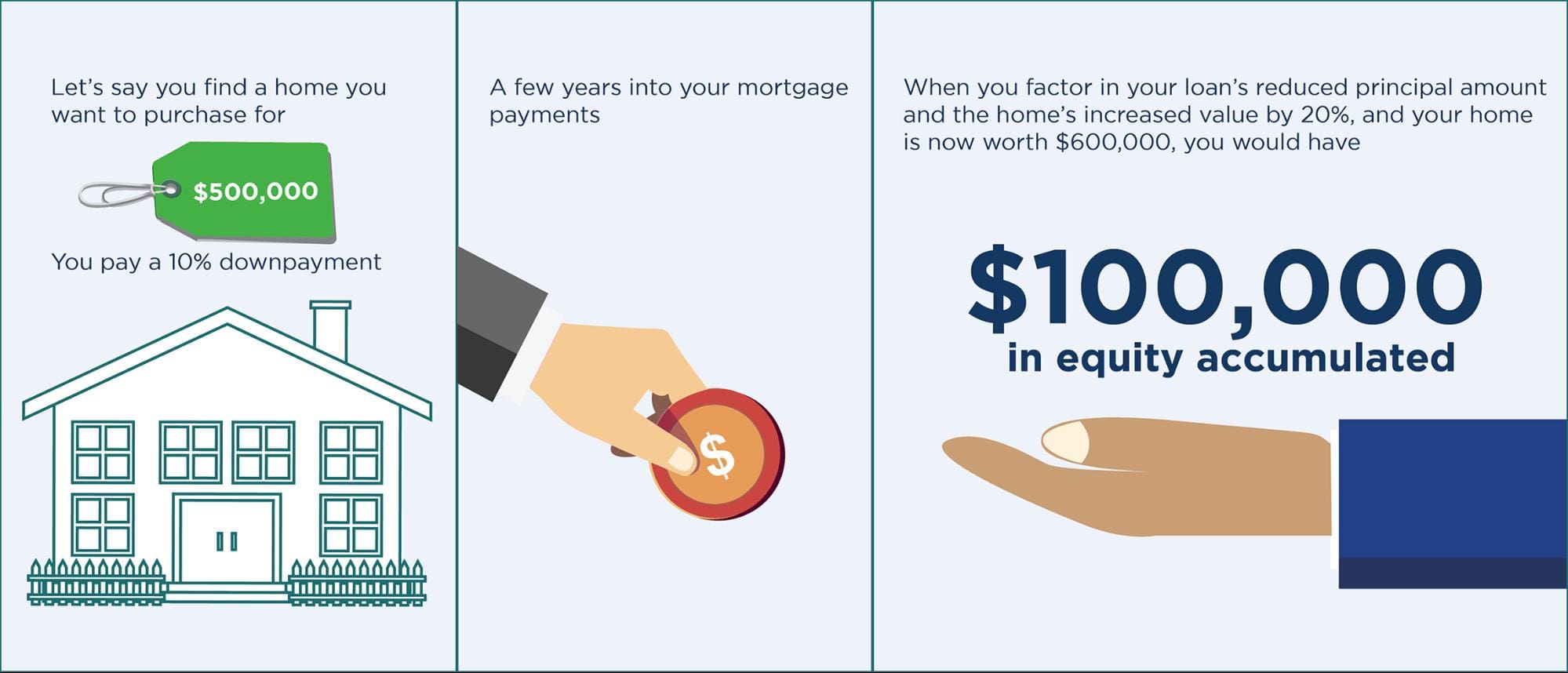

For example: Let’s say you find a home you want to purchase for $500,000, you pay a 10% down payment and are left with a $450,000 mortgage.

A mortgage is a loan you get to buy a house. A few years into your mortgage payments, as you pay off your mortgage each month, you’ve reduced the loan’s principal through your ongoing monthly mortgage payments.

At the same time, the home values in your neighbourhood have increased by 20%, and your home is now worth $600,000. When you factor in your loan’s reduced principal amount and the home’s increased value, you would have $100,000 in equity accumulated from the home appreciation as well as some $15,000 – $25,000 as a result of principal paydown (depending on your interest rate, amortization).

Can I access that home equity?

Yes. One of the primary benefits of home equity is that you don’t have to wait to sell your home to realize it.

You can leverage that home equity by borrowing against it through either a home equity loan or a home equity line of credit (HELOC). Keep in mind that by borrowing against this equity in your home, you are using your home as collateral for the lender’s security.

You will have to make interest payments on this additional loan in addition to your regular monthly mortgage payments. It’s important to budget for both payments.

HELOC vs home equity loan

With a home equity loan, you borrow a fixed amount of funds, typically secured at a variable interest rate. You would repay this loan over a set period similar to how you would pay back your mortgage on your home. Frequently, these loans are referred to as a second mortgage.

A home equity line of credit, on the other hand, works where a lender would extend you a line of credit based on your accumulated equity rather than providing you with a one-time lump sum loan.

The lender would establish a maximum line of credit and grant you access to the maximum amount calculated based on the amount of equity. You can then spend any amount at any time for any purpose until you have borrowed to the maximum. This type of loan is very beneficial and affordable since the interest that accrues on the amount that the borrower had drawn against the loan.

If you are a business owner and have a business registration, you have an additional benefit where the interest payments on your HELOC and/or second mortgage loan are tax deductible. This means that you can take out the interest payments as an expense before you declare your business profits, thus leaving you with more money as net income.

This is an excellent option for small businesses that require access to cheap forms of long-term capital.

A HELOC typically will have lower upfront costs compared to home equity loans, but it is still important to shop around and compare the different fees charged by lenders on HELOC.

For example, some lenders may charge a home appraisal fee while others may not. They will need to conduct an appraisal to verify the market value of your home that they will lend against. The terms of the HELOC may also differ according to the lender. This may include the draw period and repayment terms.

How much can you afford to borrow?

When evaluating whether to take a home equity loan, it is essential to take into consideration your monthly recurring expenses attributed towards the ownership of your home. You need to have a realistic sense as to what you can afford.

Tally up your monthly costs including your monthly mortgage payments, property taxes, insurance, utilities, home maintenance and any condominium fees if any. Now, develop a monthly budget and look at other factors that determine how much you can afford to repay.

With a monthly budget in hand, you can see how much room you have each month to afford the additional expense of taking on a home equity loan.

Many Canadians choose to carry out their home renovations with the aid of a home equity loan.

Home equity loans: Final thoughts

Home equity loans are a great option if they are used responsibly and if you budget accordingly. You may decide to take out a second mortgage to make significant improvements to your home, and in doing so, the value of your home may increase and perhaps even negate the loan that was taken out for home improvements.

Be sure to consult with a qualified mortgage professional to consider all your options, and to discuss your specific financial situation.