Global financial markets faced unprecedented disruption when economies shut down in response to the global COVID-19 pandemic. To support financial markets, the Bank of Canada launched 10 liquidity facilities and asset purchase programs. As markets recovered from the initial shock, the central bank refocused their operations from ensuring that markets functioned to using these tools for monetary policy.

Given that the Bank’s policy interest rate reached its effective lower bound of 25 basis points, quantitative easing (QE) played a pivotal role in extending the reach of interest rate reductions across the yield curve. QE involves the central bank purchasing government securities or other financial assets from the market, which increases the money supply and lowers long-term interest rates. By injecting liquidity into the financial system, QE aims to encourage lending and investment, stimulate economic activity, and support asset prices.

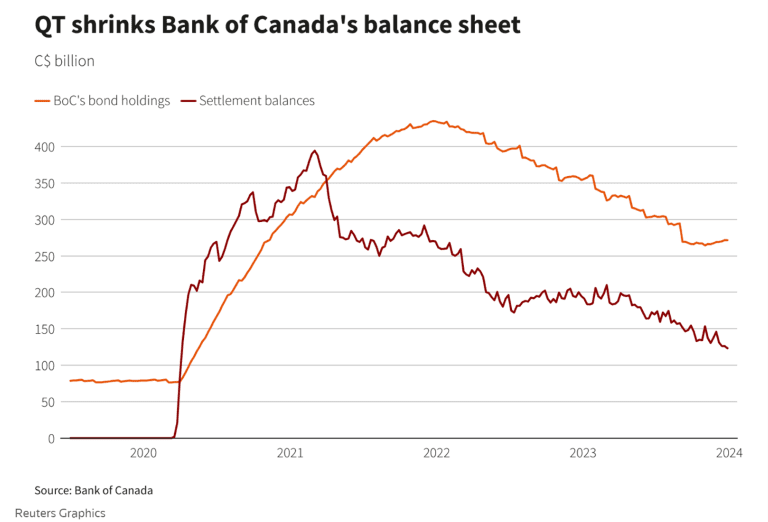

As a result, QE served as an additional tool for implementing monetary stimulus measures during the pandemic, leading to the Bank’s holdings of Government of Canada bonds reaching approximately $440 billion at its peak. However, starting from April 25, 2022, the Bank transitioned from quantitative easing (QE) to quantitative tightening (QT), allowing assets to gradually roll off its balance sheet. Last March, the Bank indicated its expectation that QT would conclude around the end of 2024.

The objective is to employ an abundant reserve system (ARS), also known as a “floor system,” for setting interest rates. Previously, the Bank had operated under a “corridor system,” which is characterized by scarce reserves. In this system, the central bank sets a policy rate, such as the overnight lending rate, which serves as the upper bound of the corridor. Simultaneously, the central bank sets a lower bound, typically referred to as the deposit rate or the floor rate. Banks can borrow funds from the central bank’s lending facility at the upper bound rate and deposit excess reserves at the lower bound rate. The corridor system effectively limits short-term interest rate fluctuations within this range, with market forces determining rates within the corridor.

Central banks typically use the corridor system to maintain control over money market rates and influence broader economic conditions. However, during times of financial stress or when interest rates approach zero – as they did during the pandemic – central banks may adjust their policy framework, such as transitioning to an abundant reserve system, to better achieve their monetary policy objectives.

Claudio Borio of the Bank for International Settlements notes, there are potential drawbacks to the abundant reserves approach. Firstly, there’s a greater need for the central bank to inject liquidity during periods of stress to maintain market stability. Secondly, it could contribute to collateral scarcity. Rates in the repo market, which is used by the bond market to finance bond portfolios, are heavily dependent on the supply of government securities and reserves.

In 2017, then Federal Reserve chair Janet Yellen likened the reduction of the Fed’s balance sheet to “watching paint dry,” suggesting it would go unnoticed. However, in practice, we saw stress events in the repo market in 2019, when increasing reserve scarcity hindered banks from lending in the money markets, leading to higher repo rates due to heightened demand for cash.

Recently, the Canadian Overnight Repo Rate Average (CORRA), the overnight repo rate between banks that serves as the Bank of Canada’s target rate for monetary policy, has traded above the Bank’s intended target of 5%. At times, CORRA exceeded the target by as much as 6 basis points, prompting the Bank to inject $5 billion of liquidity into the overnight market through its overnight repo operations.

Part of the challenge stems from the fact that although banks are able to hold large cash reserves since the financial crisis, liquidity requirements mandating banks to maintain minimum cash levels can limit their willingness to lend funds. The introduction of Lynx, the real-time payment system used by the Bank of Canada for implementing monetary policy, presents another aspect of the challenge. Lynx, which replaced the Large Value Transfer System (LVTS) in 2021 as part of Canada’s payments modernization efforts, is still in its early stages, and the amount of settlement balances required for the system is still being refined.

Settlement balances have decreased significantly, dropping to $112 billion from a peak of $390 billion in February 2021. The Bank has indicated an estimated target range for settlement balances of between $20 to $60 billion, while market analysts anticipate that settlement balances will stabilize at approximately $80 to $100 billion. Additionally, there is speculation that the central bank may signal the end of quantitative tightening (QT) as early as April.

Housing Affordability Watch

CMI monitors the latest developments and offers insights on solutions to Canada’s housing affordability crisis

Despite the presence of various rent control policies across Canada, doubts persist about their effectiveness in curbing inflation in the housing market. With rent controls in place for a significant portion of the rental market, including capped increases and annual guidelines, one would expect more stability in rental prices. However, despite these measures, the rent component of inflation remains notably high.

While rent inflation is expected to moderate, ongoing pressure exists to either tighten existing controls or introduce new ones, as seen in recent bylaws targeting renovictions. Yet, economists caution against the broader implications of rent controls, citing their potential to deter new construction, reduce housing quality, and distort market dynamics. In this context, the debate shifts towards the concept of housing abundance as the most effective form of rent control, where a surplus of housing incentivizes landlords to prioritize tenant retention over excessive rent hikes.

Read the full article here: Housing Abundance is the Best Rent Control

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any person or organization in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice including investment advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication. Readers are cautioned to always seek independent professional advice from a qualified professional before making any investment decisions.