Last week, some of the biggest names in American finance flagged emerging challenges in the credit market. JPMorgan CEO Jamie Dimon, Citi Group CEO Jane Fraser, and Apollo’s Marc Rowan each highlighted potential risks in recent statements.

Dimon opened the week with a stark warning about the private credit market, noting that “when you see one cockroach, there’s probably more,” following JP Morgan’s disclosure of a $170 million loss linked to the collapse of subprime auto lender Tricolor Holdings. Fraser warned of “pockets of valuation frothiness,” while Rowan was more pointed, suggesting in a Financial Times interview that “there’s been a willingness to cut corners.”

Bank stocks sold off aggressively across the board following disclosure from Zions Bancorp and Western Alliance Bancorp of bad loans tied to the bankruptcies of two auto lenders. Shares of investment bank Jefferies also declined this month after it revealed some exposure to bankrupt auto parts maker First Brands.

These disclosures are the latest in a series of developments that have captured Wall Street’s attention as investors look for signs of credit deterioration among commercial borrowers. That said, despite these pockets of concern over bad loans at regional U.S. banks, there’s little evidence of a broader, systemic problem.

Non-bank lenders, which stepped in to provide loans that banks stopped underwriting after the Great Financial Crisis, have grown immensely since the bottom of the crisis. Today, private credit is not only competing with banks on higher-risk loans but also issuing multi-billion-dollar loans to investment-grade clients.

The private credit market overall appears well positioned, despite some recent jitters. Hamilton Lane, a global leader in private markets investing, regularly publishes research and insights on private equity and private credit, helping investors understand trends and risks in these markets. In a review of the market this spring, the firm highlighted three key points:

- “A significant funding gap exists between the amount of buyout dry powder and credit origination dry powder, suggesting a supply-demand imbalance.” This indicates that demand for private credit remains strong, reducing the risk of lenders chasing deals.

- “Private credit has demonstrated positive vintage year IRR for the past 23 years and has historically outperformed its public market equivalent.”

- “Defaults remain inside the long-term average.”

While private credit markets in the U.S. and Europe are experiencing a slight reset, the question is: how is the Canadian market faring?

Canada’s Private Credit Market

Compared to the U.S., Canada’s private credit market is smaller and lacks the same securitization takeouts—a process where lenders package and sell their loans to transfer credit risk and free up capital. As a result, it operates more as a buy-and-hold market, with lenders retaining the credit risk. Still, there are still risks that investors need to be aware of.

In Canada, risks to private mortgage credit are largely tied to domestic macroeconomic and policy trends. So far, these factors have created some pressure points but not significant fractures in the housing market.

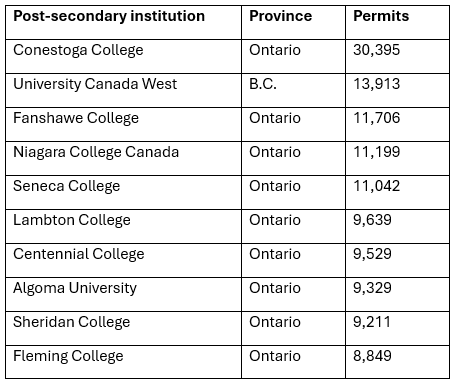

One area drawing attention recently is immigration. Increased inflows of newcomers, including international students, have driven investor activity in condos and rental properties, often through the addition of basement suites. Much of this demand has been concentrated in markets serving international students, as seen in the chart below.

Top 10 List: Study Permits for International Students in 2023

Source: CBC analysis of Immigration, Refugees and Citizenship Canada data tables

Foreign student recruitment in Ontario rose sharply in 2018 and accelerated further after the provincial government froze post-secondary funding in 2019. The federal government then imposed a cap on study permits in 2024.

Between January and June 2024, Canada issued 125,034 international study permits. Over the same period in 2025, that number dropped to 36,417, according to Immigration, Refugees and Citizenship Canada (IRCC).

This shift has had a twofold impact. First, declining international enrollment has led many colleges and some universities to cut staff and programs, particularly those heavily reliant on international students. The drop in enrollment has also reduced demand for nearby student housing. At Conestoga and Sheridan, for example, most international students were based in Brampton and Mississauga, often renting basement suites, apartments or condos. The sudden decline in demand has created challenges for investors who purchased existing or pre-construction small rental units in these markets, only to see the anticipated demand disappear.

The second major impact has been on the condo market, driven by restrictions on foreign buyers and short-term rentals. The foreign buyer ban curbed preconstruction demand in major cities, particularly Vancouver. Meanwhile, limits on short-term rentals, intended to increase long-term rental supply, have had unintended consequences for micro-condo units. Many of these 300-400 square foot condos in cities like Vancouver, Toronto and Victoria were originally purchased for short-term rental income from tourists and other visitors. With short-term rentals now restricted, the units are often not attractive as permanent long-term housing, contributing to an oversupply. Given the limited pace of new condo construction, however, I expect the imbalance to be temporary.

The broader macroeconomic picture makes it difficult to pinpoint exactly where specific impacts will be felt. Trade issues have put pressure on sectors such as forestry, steel, auto, transportation and warehousing, and aluminum. Some of these sectors, like forestry and aluminum, are concentrated in more rural and remote regions, where private mortgage credit activity tends to be limited.

One might expect the steel industry to see a broader decline, but the impact has been more localized, affecting regions such as Sault Ste. Marie more than Hamilton. In September, Hamilton’s total employment fell by 3,000 after a period of strong growth earlier in the year. The city’s unemployment rate is now above last year’s level and slightly higher than the national average.

Ontario overall has experienced significant manufacturing job losses. In the second quarter of 2025, the province shed 29,400 positions. Since Toronto accounts for the largest share of Ontario’s manufacturing jobs, it is not surprising that the GTA now has the highest unemployment rate in the province.

Through 2025, the auto sector has seen declines in specific areas, particularly motor vehicle parts manufacturing. Conversely, employment in motor vehicle assembly has experienced a modest increase, and the auto dealer and repair sectors are up.

However, a few key plants are currently shut down for retooling. Ford’s Oakville plant is expected to remain closed until 2026, while the Stellantis plant in Brampton has been shut down since early 2024. Work there was temporarily halted in February when the U.S. rolled out tariffs aimed at boosting domestic auto production. Stellantis has indicated its intention to move the long-planned Jeep production out of Ontario, putting 2,200 jobs at risk. That said, the company still intends to run a third shift at its Windsor assembly plant, and it remains too soon to determine whether new production in Brampton will proceed, as it depends on a renewed free trade agreement.

The next key development will be the federal budget and any measures it may introduce to restructure the economy and support affected sectors. How these policies unfold will influence employment, housing demand, and the broader lending environment.

Housing Affordability Watch

CMI monitors the latest developments and offers insights on solutions to Canada’s housing affordability crisis

CMHC is unique among federal entities. As a Crown corporation, it manages commercial mandates like mortgage insurance and securitization, while also delivering federal policy initiatives in social housing. This unique role has made CMHC central to Canada’s housing system—but it has also created complexity, overlapping responsibilities, gaps in accountability, and sub-par outcomes.

Our latest Housing Affordability Watch explores why restructuring CMHC could streamline policy delivery, improve housing outcomes, and allow the agency to focus its efforts where they matter most: promoting a stable, efficient housing market.

Read it here: CMHC – Why It’s Time to Rip of the Band-Aid

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any person or organization in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice including investment advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication. Readers are cautioned to always seek independent professional advice from a qualified professional before making any investment decisions.