Canada’s economy is growing at its slowest rate in 60 years, with only housing preventing things from getting worse.

Canada’s economy has seen better days. Gross domestic product, a measure of all the goods and services produced in the economy, is expanding at its weakest rate in 60 years.[1] What’s worse, the outlook isn’t expected to improve anytime soon. Increasingly, housing is seen as Canada’s only source of strength in an otherwise moribund environment.

Canada Experiences Worst Month in Over 7 Years

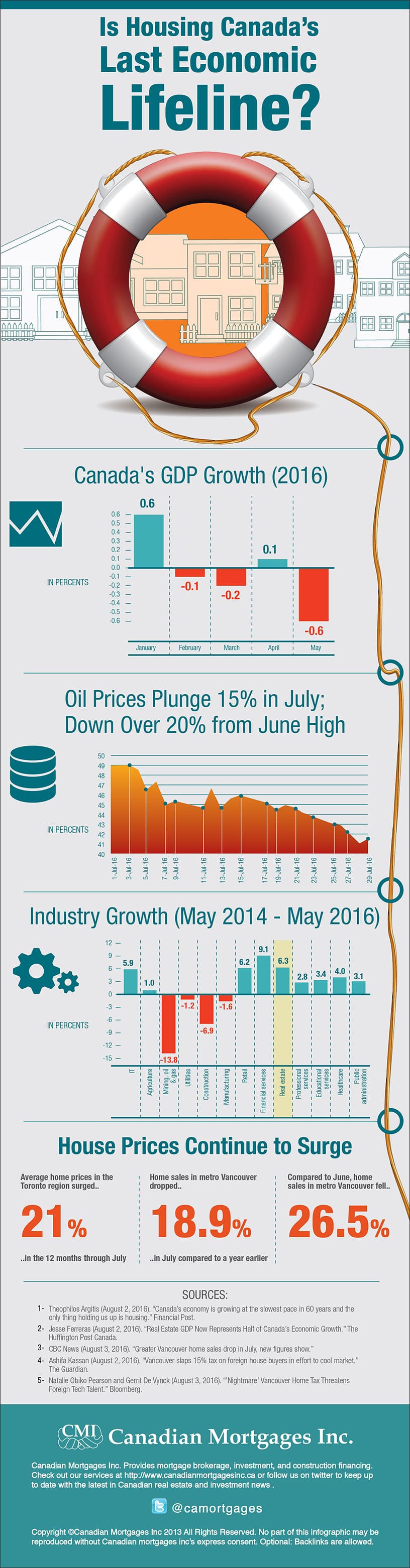

The Canadian economy shrank 0.6% in May, as wildfires ravaged the oil-producing region of northern Alberta, cutting crude production by 22%. The monthly contraction in GDP was the worst in more than seven years. (Refer to the infographic for Canada’s GDP growth over the past five months.)

It wasn’t just oil and gas that took a beating. Manufacturing and utilities also declined sharply. Services increased, but weren’t enough to offset the huge declines in goods-production.

According to economists, the worst is still yet to come.

Oil Prices Plumb New Lows

The renewed drop in oil prices has many concerned that Canada could re-enter recession this year. Oil prices have plunged more than 20% from the June highs, meeting the technical definition of a bear market. Since reaching highs north of $51 a barrel in June, WTI crude futures would plunge as much as 23% two months later.

Brent crude, the international futures benchmark, is also down nearly 20% from its June highs.

Real Estate Represents Half of Canada’s Economic Growth

If there was any doubt that real estate is the stalwart of Canada’s economy, the next figure should set you straight. While real estate accounts for only about 12.5% of the economy, it has been responsible for half of the economy’s growth since the oil-price collapse began over two years ago.[2]

Canada’s real estate sector grew 6.8% in the two years through May, far outpacing virtually every other sector. By comparison, manufacturing declined 2.4% over the same period. Oil and gas has tumbled 14% in the 24 months through May (refer to infographic for full breakdown).

While financial services outpaced real estate in terms of growth, it should be mentioned that much of the growth in bank lending over the past two years has been used to finance home buying and real estate development.

Canada’s economy as a whole expanded a mere 1.2% over the last two years. The Bank of Canada (BOC) is warning of sharper declines this summer as the market rebalances from the Alberta wildfires.

The BOC expects the Canadian economy to expand just 1.3% this year, down from the April estimate of 1.7%. Growth is forecast to pick up to 2.2% in 2017 and 2.1% the year after that.

House Prices Continue to Surge

Average home prices in the Toronto region surged 21% in the 12 months through July, reaching a staggering $952,983, the Toronto Real Estate Board recently announced. Locals are concerned that prices will continue to skyrocket as more investors make their way to Toronto after British Columbia imposed a new 15% tax on foreign buyers in metro Vancouver.

“There is evidence now that suggests that very wealthy foreign buyers have raised the price, the overall price of housing for people in British Columbia,” BC Premier Christy Clark said.

The new measures appear to have worked, at least initially. Home sales in metro Vancouver dropped 18.9% in July compared to a year earlier. Compared to June, home sales fell 26.5%.[3] However, analysts warn that it’s still too early to tell how the new measures will impact home buying in the region.

The average home price of a detached home in metro Vancouver has reached $1.56 million, up 39% from a year ago.[4]

However, experts warn that the new tax could have unintended consequences, such as limiting business investment in the region. The 15% levy adds a third strike against a city already struggling with some of the highest housing costs and lowest wages in North America’s technology industry.[5]

References

[1] Theophilos Argitis (August 2, 2016). “Canada’s economy is growing at the slowest pace in 60 years and the only thing holding us up is housing.” Financial Post.

[2] Jesse Ferreras (August 2, 2016). “Real Estate GDP Now Represents Half of Canada’s Economic Growth.” The Huffington Post Canada.

[3] CBC News (August 3, 2016). “Greater Vancouver home sales drop in July, new figures show.”

[4] Ashifa Kassan (August 2, 2016). “Vancouver slaps 15% tax on foreign house buyers in effort to cool market.” The Guardian.

[5] Natalie Obiko Pearson and Gerrit De Vynck (August 3, 2016). “’Nightmare’ Vancouver Home Tax Threatens Foreign Tech Talent.” Bloomberg.