Canadians are feeling the squeeze of high housing costs, and the debate over affordability is intensifying. Recently, Federal Housing Minister Gregor Robertson suggested that average house prices need to fall to restore affordability. But what does “affordable” really mean, and how can prices realistically adjust?

Housing affordability is typically measured by comparing shelter costs—including mortgage payments, property taxes, and utilities—to household income, with a common benchmark that these costs should not exceed 30 per cent of household income. Home prices factor into this calculation through mortgage payments. Lower home prices can improve affordability—but so can higher incomes or lower mortgage rates. The challenge is that falling home prices can create negative wealth effects for current homeowners.

For Canadians who rent, particularly those in lower income brackets, a metric based on ownership costs does little to reflect their experience of affordability. Minister Robertson emphasized that “[w]e have to build a lot more non-market housing to bring down that average cost.” His definition of affordability is clearly different from traditional metrics – it includes rental housing (the CMHC model that estimates the supply needed to improve affordability also accounts for the rental sector).

The National Housing Strategy has focused primarily on renters rather than homeowners. Much of this effort has focused on funding two key programs: the Apartment Construction Loan Program and the MLI Select program for multifamily mortgage insurance. While increased activity in apartment rentals has led to some decline in rents, vacancy rates remain tight in most markets.

Significant work remains to address housing for homeless individuals. It is unclear how much of the $13 billion promised for Build Canada Homes will go toward deeply affordable housing, supportive housing, Indigenous housing, and shelters. Progress is being made in building more deeply affordable rental housing, but social rental units still account for only about 3.5 per cent of the total housing stock.

For Canadians who are or hope to become homeowners, the path to lower home prices is not so clear. Measures such as removing the HST on new housing would certainly help, as would getting individual municipalities on board to reduce their development charges. The Liberal platform called for “cut[ting] municipal development charges in half for multi-unit residential housing,” but similar support does not exist for single-family homes.

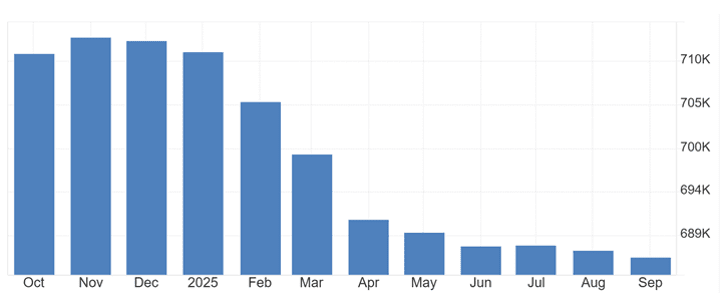

Home prices have declined in some markets—most notably in Ontario—from their 2022 peak. This is largely an unwinding of the pandemic-era housing bubble. In other regions, such as Alberta, Atlantic Canada, and Quebec, prices have continued to rise. The national average has edged lower mainly due to the downward pressure from Ontario and British Columbia.

Average Canadian House Prices

Source: Canadian Real Estate Association (CREA)

I expect the government’s messaging on housing affordability will remain vague. It wants to claim that house prices are falling as evidence of progress. Rental markets may see modest declines in rents, but that doesn’t mean home prices are actually falling in most markets. This is not the message prospective homebuyers want to hear—unless they’re willing to look to markets such as Alberta or Atlantic Canada, where typical home prices remain below the national average.

For most Canadians, affordability challenges persist, and falling prices alone won’t make homes truly accessible.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any person or organization in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice including investment advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication. Readers are cautioned to always seek independent professional advice from a qualified professional before making any investment decisions.