Central banks control the front end of the yield curve—market yields on bonds maturing in a few years or less—while the back end, covering bonds maturing in 10 years or more, reflects expectations for growth and inflation. In Canada, the US bond market also plays a role, as our domestic market often takes direction from the larger US market.

In the near-term, the short-end of the US yield curve suggests that the Fed is likely to cut its policy rate at most twice this year.

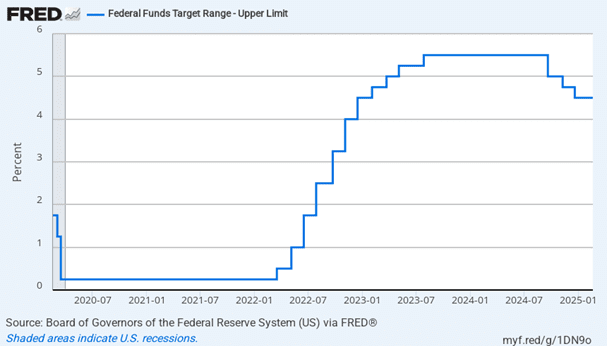

At its January 2025 meeting, the Federal Open Market Committee (FOMC) held the federal funds target rate steady at 4.25 per cent to 4.50 per cent. This follows three consecutive rate cuts at the end of last year, totaling a full percentage point. At its previous meeting in December, FOMC members signalled a more cautious approach, trimming projected 2025 rate cuts from four to two.

Source: Federal Reserve Economic Data | FRED

In a statement after the January meeting, the Fed noted that risks to its dual mandate of full employment and low inflation are “roughly in balance.” It acknowledged ongoing economic uncertainty and emphasized its attentiveness to risks on both sides of its mandate.

Justifying its decision to hold rates steady, the Fed stated, “Economic activity has continued to expand at a solid pace (with Gross Domestic Product growing at a 3 per cent rate in mid-2024).[1] The unemployment rate has stabilized at a low level in recent months (4.1 per cent in December 2024) and labor market conditions remain solid.[2] Inflation remains somewhat elevated (2.9 percent in December 2024).”[3] Citing current economic conditions, Fed Chair Jerome Powell added, “We do not need to be in a hurry to adjust our policy stance.”[4]

Since that meeting, core inflation rose 0.45 per cent month-over-month in January, exceeding the 0.3 per cent expected and accelerating from December’s 0.2 per cent. Much of that rise was driven by services. This pushed the three-month annualized core inflation rate to 3.9 per cent— well above the Fed’s 2 per cent target and more in line with the strength seen in wage growth.

This data underscores the cautious tone expressed by some Fed governors in recent months. Federal Reserve Bank of Atlanta President Raphael Bostic scaled back his forecast to potentially just one rate cut. Federal Reserve Bank of Minneapolis President Neel Kashkari raised the prospect of no cuts this year, while Fed Governor Christopher Waller sees no urgency in lowering the policy rate given the strength of the incoming economic data. Fed Governor Miki Bowman was the first to hint at the potential for another rate hike, and in a speech last week, Fed Governor Michelle Bowman highlighted the need for more inflation data before advocating for additional interest rate cuts.

What is the bond market signalling?

Bond traders are concerned with more than just the front end of the curve. They also focus on the supply of bonds, inflation expectations, and the outlook for growth.

During the pandemic, the Fed attempted to stimulate economic activity by purchasing fixed income assets, including US government bonds and agency mortgage-backed securities. While the Fed’s market participation helped moderate interest rates, it also grew its assets to nearly $9 trillion by 2022. Since then, the Fed has been reducing its holdings, bringing its balance sheet down to less than $7 trillion.[5]

The Fed is currently allowing up to $25 billion per month in Treasuries and $35 billion per month in mortgage bonds to run off its balance sheet. This pace marks a decrease from the previous $60 billion per month in Treasuries as of June 2024. Initially, many expected this runoff to end by March 2025, but expectations have since shifted to June 2025 or later. The Fed’s reduced bond market participation may be contributing to the elevated interest rates we’re seeing today. For instance, 10-year US Treasury yields rose from a low of 3.63 per cent in September 2024 to 4.55 per cent in late January 2025.

Part of the rise in long-term rates can also be attributed to higher inflation expectations, along with the anticipated increase in federal deficits. However, the most significant driver is the deep uncertainty surrounding the administration’s actions on tariffs, immigration and the federal budget, as well as the knock-on effect this uncertainty has on the Fed’s willingness to continue easing monetary policy.

While these policy moves have broad political, geopolitical and social implications, the greater concern for investors is the uncertainty they create. Investors must consider how these actions, and the uncertainty surrounding them, could slow economic growth.

We believe that rates will stay higher for longer, with increasing uncertainty leading to greater rate volatility.

[1] Source: U.S. Bureau of Economic Analysis

[2] Source: U.S. Bureau of Labor Statistics.

[3] Federal Reserve Board of Governors, “Federal Reserve issues FOMC statement,” Jan. 29, 2025.

[4] Federal Reserve Board of Governors, “Chair Powell’s Press Conference,” Jan. 29, 2025.

[5] Board of Governors of the Federal Reserve System (US), Asset: Total Assets: Total Assets (Less Eliminations from Consolidation), retrieved from FRED, Federal Reserve Bank of St. Louis. As of January 22, 2025.

Housing Affordability Watch

CMI monitors the latest developments and offers insights on solutions to Canada’s housing affordability crisis

Efforts to expand Canada’s mortgage securitization market have been ongoing for years, but meaningful progress has yet to materialize. To build a more active, investor-friendly market, a new approach is needed—and Canada’s national housing agency has an essential role to play.

Explore how CMHC could lay the groundwork for a thriving mortgage securitization market in Canada in our latest Housing Affordability Watch: Building a Strong Foundation for a Canadian Mortgage Securitization Market

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any person or organization in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice including investment advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication. Readers are cautioned to always seek independent professional advice from a qualified professional before making any investment decisions.