The Bank of Canada is seeing the economy performing better than expected with inflation remaining higher than desired. The Bank moved off the sidelines last month and raised rates by 25 basis points. The question is, will the Bank raise the overnight rate by another 25 basis points this month? Below we look at the most recent data releases to get a sense of what the Bank might do.

Employment – Not shedding jobs fast enough

The Canadian economy shed 17,300 jobs in May, the first decline in nine months. This came as a surprise to analysts who were expecting the economy to add 23,000 jobs last month. The number of employees held steady in the private and public sector, while there was a decline in the number of self-employed workers (-40,000). The unemployment rate ticked up to 5.2%.

Inflation – Core measure remains sticky

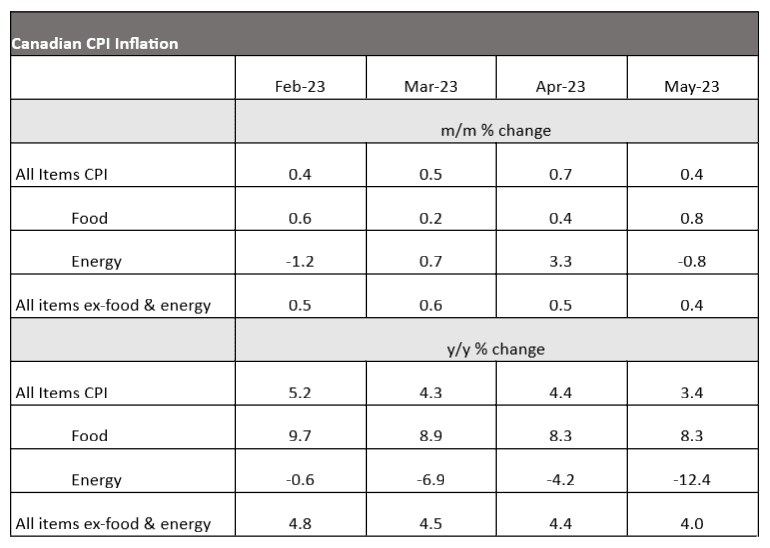

After the surprise increase in inflation in April, headline inflation slowed to 3.4% year-over-year in May. Lower energy prices drove over 60% of the decline. The Bank’s preferred CPI-trim and median measures both eased substantially in May to 3.8 and 3.9%, respectively, year-over-year, on relatively small 0.2% one-month increases from April.

Headline inflation in June is likely to fall further – potentially to the top end of the Bank’s 1-3% target range – driven by a year-over-year decline in energy prices. Getting to the Bank’s 2% target will be the challenge. While progressing lower, the underlying inflation trend is still running well above this target.

Source: Statistics Canada

Mortgage interest costs and home rent prices continue to be a major contributor to CPI growth. Inflation for mortgage interest costs in May was the highest on record at 29.9%. We expect that these costs will continue to rise as higher interest rates gradually flow to household mortgage payments. While consumers are being squeezed, the question is whether the Bank feels that further belt tightening is required.

Business Outlook Survey – Trending in the right direction

The Bank of Canada Q2 Business Outlook Survey shows an easing in sentiment. The factors highlighted in the Bank’s June policy statement all improved: lower expected price increases, easing wage pressures, waning excess demand, and lower inflation expectations.

GDP – Below consensus but still positive

After an increase in March, GDP was flat in April, falling short of market expectations. While the federal public sector strike was partly responsible for the weak performance, GDP excluding federal government output grew only 0.1%. In April we saw declines in several private sector industries – management, wholesale trade, and agriculture. Interest rate sensitive sectors such as real estate and non-residential construction improved. Residential construction continued its ongoing six-month decline.

The flash estimate for May (+0.4%) is driven by a return of the federal public sector and improvements in manufacturing and wholesale trade. Assuming the May estimate holds and June is flat, Q2 GDP would be 1.4% – higher than the Bank of Canada’s recent forecast of 1.0% . This would support the Bank’s decision to raise rates, but ongoing population growth has certainly raised potential growth much higher than had been expected.

Overall, while this data suggests the economy is losing momentum, we expect that the Bank will hike the overnight rate by 25 bp on July 12 before stepping back to the sidelines for the rest of the year.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any person or organization in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice including investment advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication. Readers are cautioned to always seek independent professional advice from a qualified professional before making any investment decisions.